The deal window just swung open again

Hi there

I have been watching the deal flow this month with the same feeling I get when the tide turns. After a long stretch of buyers sitting on their hands, the cheque books are open again, and the sizes are not small. What interests me is not the headline numbers but the pattern underneath them, because a busy market is a useful mirror. It shows you exactly what buyers value when they finally decide to move.

Enjoy!

Your subscriber-only early access to the Exit Mode Toolkit

Before I get into this week’s nuggets, here’s a bonus for all you valued subscribers. I am about to open the Exit Mode Toolkit to the public. This is the full suite of tools I use to get a business ready for sale and to pressure-test what it is worth long before a buyer ever does. There’s a custom GPT, a target company finder, a deal structure simulator, an exit readiness scorecard plus dashboards, frameworks, templates and more.

As a reader you get early access ahead of the public launch: lifetime access for a one-off $99 – this is ridiculously good value. If you want to level up your M&A game, these tools will give you an edge. There’s also three freebies to allow you to dip your toes in. Check it here.

The internet is not your customer base, and a campaign just proved it

At Cannes this week, Stagwell’s Mark Penn and American Eagle’s Craig Brommers made a point I wish more leaders would absorb: marketers keep mistaking online uproar for public opinion. Drawing on Harris Poll data and the Sydney Sweeney campaign, they showed how a campaign can be loudly condemned online and steadily loved at the till. The people shouting are rarely the people buying. For founders this is bigger than marketing. It is a warning about every signal you act on, because the loudest feedback is almost never representative, and steering by it is how good decisions go wrong. Read the article here.

AbbVie spending eleven billion tells you what scarcity is worth

AbbVie is buying Apogee Therapeutics for 10.9 billion dollars, its biggest deal in more than five years, mostly to own one late-stage eczema drug. That is the whole logic. Not a sprawling portfolio, not synergy spreadsheets, a single asset that is hard to replicate and sits dead centre of where the buyer wants to grow. It is a clean reminder that buyers do not pay premiums for size. They pay for the thing they cannot easily build themselves. For founders, the question worth sitting with is simple: what do you own that a serious acquirer could not just go and make? Read the article here.

Tropicana proves a brand is never too old to mean something new

Tropicana, a 75-year-old juice brand, has launched a global platform called Give Life Some Juice, moving deliberately beyond its orange-juice-at-breakfast box. It is a smart piece of repositioning, because the brand was not broken, it was just narrow. The risk with any heritage brand is that it slowly becomes a category footnote while the world moves on around it. The move here is not reinvention for its own sake, it is widening the meaning of the name before the market does it for you. Worth a look if your business is known for one thing and you suspect it could stand for more. Read the article here.

A take-private deal closing is the signal, not the announcement

Clearwater Analytics has just completed its 8.4 billion dollar take-private by Permira and Warburg Pincus. Announcements are cheap, but a deal of that size actually closing tells you the private equity machine has the confidence and the financing to follow through. Take-privates happen when smart money decides a business is worth more out of the public glare, away from quarterly theatre, with room to be reshaped. If you run a private company, this is the less visible half of the market coming back to life, and it is the half most likely to come knocking on a business your size. Read the article here.

The AI jobs panic is being replaced by something more useful

S&P Global’s latest read on AI and the labour market lands on a calmer conclusion than the headlines: companies are mostly adopting AI to lift productivity and revenue, not to cut headcount, and the net effect looks more like redistribution of work than elimination of it. That matters for how you plan. The owners getting real value are not the ones chasing dramatic layoffs, they are the ones steadily raising what each person can produce. AI is showing up as leverage on good people, not a replacement for them. Read the article here.

When a strategic buyer pays a premium, it is buying time

Merck KGaA has put a 73-dollar-a-share cash offer on the table for Bio-Techne, a profitable business that has grown sales around ten per cent a year for a decade. The German group is not buying a turnaround, it is buying a decade of compounding it would rather not wait to build. That is the difference a strategic buyer pays for: not assets, but the years it saves by not starting from scratch. The lesson for owners is that consistency is itself an asset. Boring, reliable growth, repeated long enough, becomes the most expensive thing on the table. Read the article here.

You give great advice to everyone except yourself

Big Think has a lovely piece on Solomon’s Paradox, the well-documented quirk that we reason far more wisely about other people’s problems than our own. Founders live inside this trap. You could coach a peer through their pricing or hiring decision in five clear minutes, then agonise over the same call in your own business for a fortnight. The fix is mechanical, not mystical: create distance. Ask what you would tell a friend in your exact position, and act on that answer. Your judgement is fine. It is your proximity to the problem that warps it. Read the article here.

AI prompt of the week: the buyer’s-eye review

A busy deal market is a good prompt to look at your own business the way an acquirer would, before one ever does. Most owners are too close to see what is genuinely valuable versus what just feels important day to day. This prompt borrows an outsider’s eyes. Paste in a short description of your business, your numbers if you have them to hand, and your honest sense of where the risks sit, then let it push back.

You are an experienced acquirer evaluating my business for purchase. Here is a description of what we do, how we make money, who depends on me, and where I think the weaknesses are: [paste]. Assess me the way you would in a real deal. First, tell me what is genuinely attractive here and why a buyer would pay a premium for it. Second, identify the three biggest value risks you see, especially anything that depends too heavily on me personally. Third, tell me which of those risks I could realistically reduce in the next twelve months, and roughly what that would do to how a buyer perceives the business. Be direct. I would rather hear the hard version now than from a buyer later.

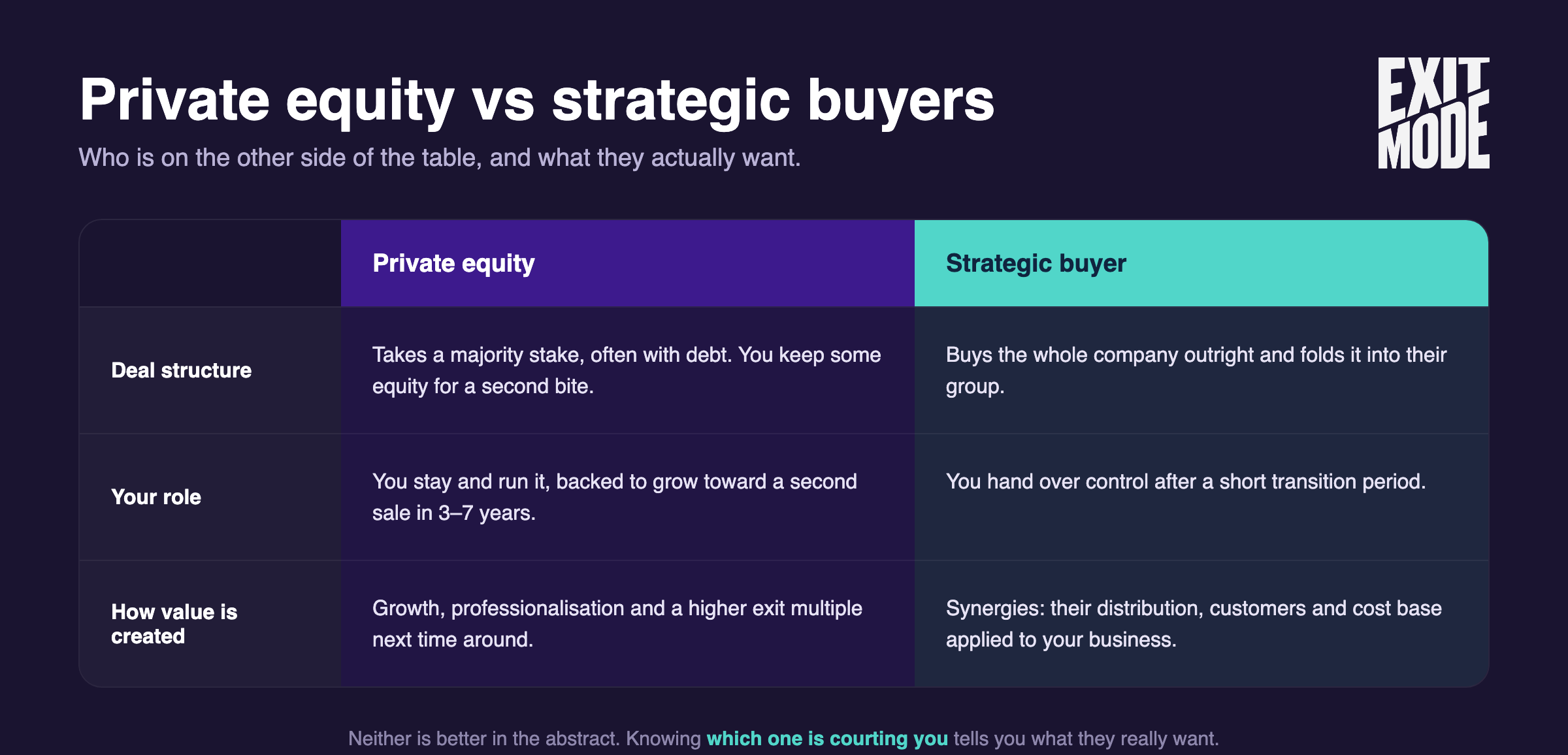

Framework: private equity versus strategic buyers

A busy market means more founders will field approaches, and the first thing worth knowing is who is actually on the other side of the table. A strategic buyer usually wants all of it: they buy the whole company, fold it into their group, and you hand over control after a short transition, with the price reflecting the synergies they expect to capture. A private equity buyer typically takes a majority stake, keeps you running the business, and backs you to grow it toward a second sale in three to seven years, which means partial cash now and a potential second bite later. Neither is better in the abstract. They suit different founders at different moments, and knowing which one is courting you tells you what they really want. The graphic below lays the two side by side across deal structure, your role, and how each one creates value.

Drop me a line

A busy market is a good moment to ask yourself the buyer’s question even if you have no intention of selling, because the answer makes the business stronger either way. If a deal has ever crossed your desk, or you have wondered what yours might be worth, hit reply and tell me. I read every message and it shapes what I write here.

Cheers!

Adam