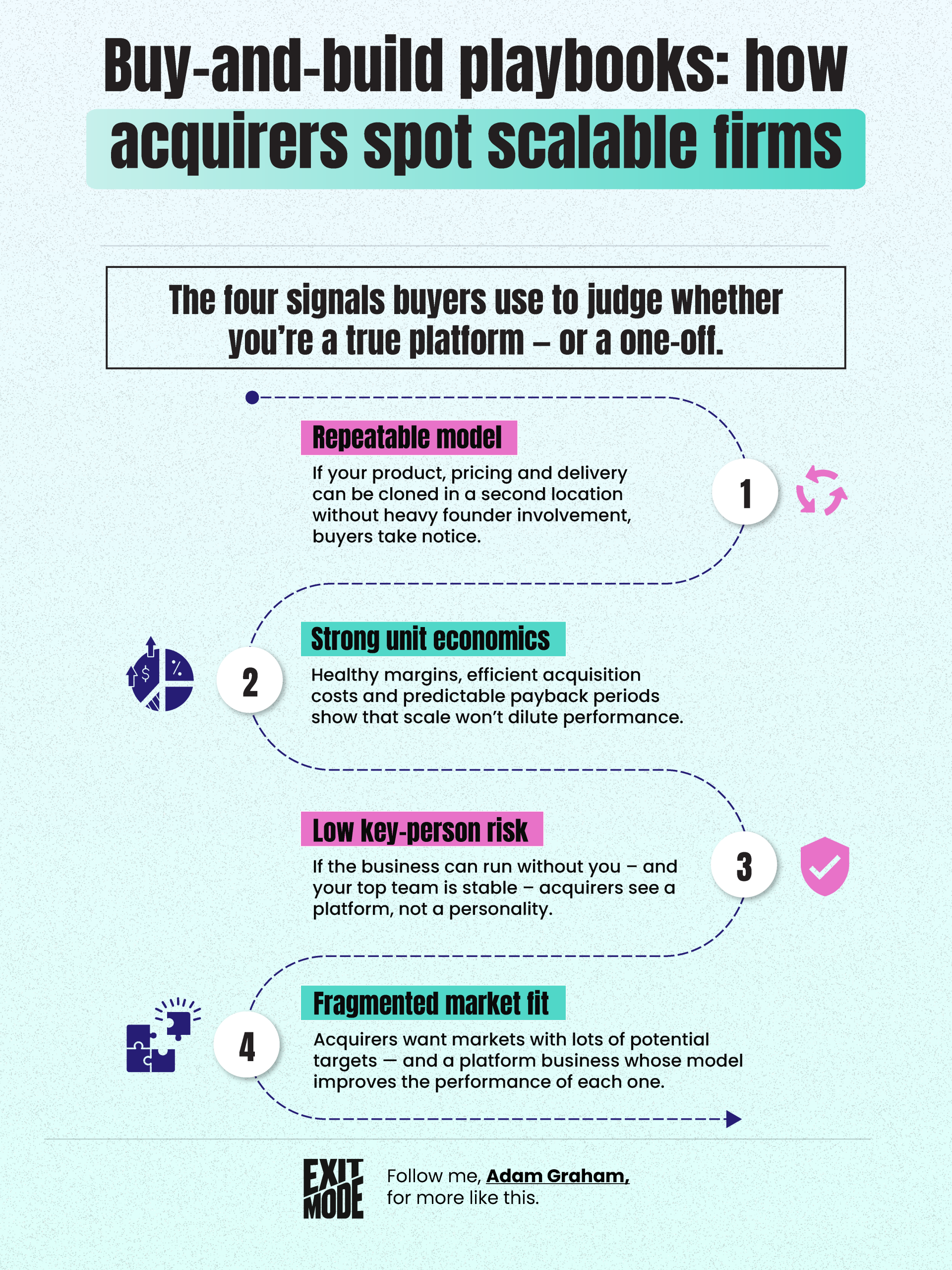

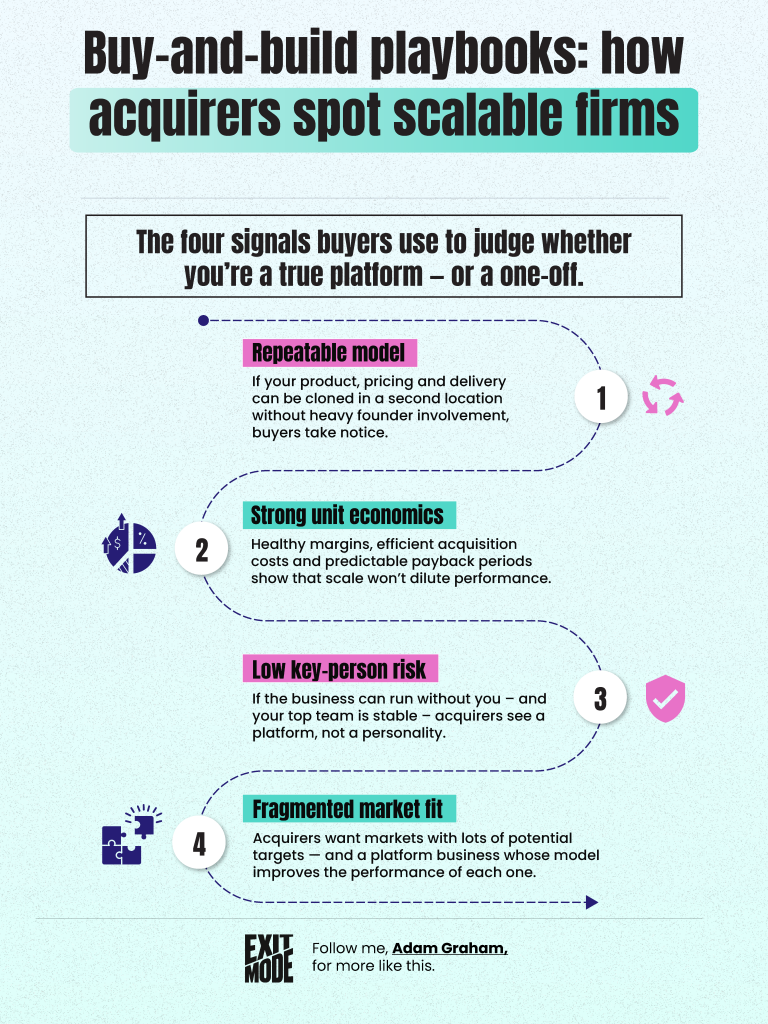

The four signals buyers look for

Hi there

A good Sunday morning to you. There is a pattern running through the week’s news that is hard to miss: capital is on the hunt. Private equity is buying up high-street names, professional-services firms are rolling up their smaller rivals, and the question for any owner is no longer “will someone want this?” but “what makes them want it enough to pay a premium?” A few things to chew over with your morning brew.

Enjoy!

Private equity keeps buying the British high street

Modella Capital sealed its takeover of Flying Tiger Copenhagen this week, adding the quirky homeware chain and its roughly 1,000 stores worldwide (80 in the UK) to an empire that already includes the former WH Smith high-street stores and Claire’s Accessories. It is the latest in a run of private-equity swoops on British retail. The interesting part for owners is the appetite, not the names. When buyers are this active at the top of the market, the demand filters down to the next tier and the one below that. A firm that could not get a meeting two years ago is now fielding approaches. If you have been telling yourself “in a few years”, the few years just got shorter. Read the article here.

A founder finally admits the expansion was a mistake

Guzman y Gomez co-founder Steven Marks has pulled the plug on a six-year push into the United States, closing the Mexican food chain’s venues in the Chicago area at a cost of up to US$40m, just months after insisting a breakthrough was close. The market rewarded the retreat: the shares jumped sharply on the news. There is a hard lesson here about sunk cost. Marks spent years dismissing shareholder concerns that the US drag was hurting the core Australian business, and the moment he stopped defending it, value returned. Knowing when to kill a project you have championed in public is one of the least celebrated and most valuable skills an owner has. Read the article here.

When a brand survives but the company does not

Radley, the British handbag maker, has been bought out of administration by Gordon Brothers in a pre-pack deal that secures the brand and its intellectual property while leaving the UK store estate at risk. It is a reminder that “the brand was saved” and “the business was saved” are two very different sentences. Buyers in distressed situations are increasingly happy to acquire the name, the customer list and the IP, and walk away from the leases, the staff and the liabilities. For owners, the uncomfortable read-across is that the equity in your brand and the equity in your company can part ways at the worst possible moment. The time to separate and protect the valuable assets is long before you ever need to. Read the article here.

The deal where a company was sold and went shopping on the same day

Here is a neat one. UK entertainment-research firm Ampere Analysis was acquired by private equity firm Goldenpeak and, on the very same day, used its new backing to buy a rival, PlumResearch. It is the cleanest illustration I have seen this month of why founders sell to private equity in the first place. The point is rarely just the cheque. It is the firepower that comes with it: the ability to go from being a target to being an acquirer overnight. If you have ever framed a sale as “the end”, this is the counter-example. For the right owner, selling a stake is the start of a far more ambitious chapter. Read the article here.

Specsavers changes its line for the first time in 22 years

Specsavers has evolved “Should’ve gone to Specsavers” for the first time in over two decades, broadening the platform beyond eye tests and hearing checks toward a wider care story. Twenty-two years is an extraordinary run for a single line, and the lesson is not that consistency is boring, it is that consistency is the asset. Most owners change their marketing message because they are bored of it, long before the market is. The brands that compound are the ones that resist the itch to reinvent and instead stretch what they already own. When Specsavers does finally evolve, it does so from a position of enormous accumulated recognition that newer rivals would pay almost anything to buy. Read the article here.

SAP’s bet on AI that runs whole processes, not single tasks

SAP set out its view of the next phase of business AI this week, and the framing is worth borrowing. The shift it describes is away from automating individual steps and toward AI that runs entire processes end to end, freeing people from coordination work so they can concentrate on judgement, oversight and strategy. That is the right lens for any owner deciding where to point AI in their own business. The low-value wins are the bits of work that only move information from one place to another. The high-value play is handing over a whole repeatable process and keeping your people for the parts that need a human to decide. Read the article here.

The risk hiding inside your rush to adopt AI

Francis deSouza, COO of Google Cloud, gave a warning this week that every owner racing to roll out AI should pin up. The danger he flagged is “shadow AI”: staff reaching for consumer tools on their own, with no oversight, no governance, no audit trail. “Security is not something you can bolt on later, and it’s not something you can leave up to employees to do on their own,” he said. The detail that should make you sit up: the average time from a breach to the next stage of an attack has fallen from eight hours to 22 seconds. AI agents also surface old data nobody remembers, those forgotten servers and stale permissions. The lesson is not to slow down on AI. It is to put the guardrails in before, not after, your people run ahead of you. Read the article here.

The Bank of England is holding, and that tells you something

The Bank of England has kept the base rate at 3.75 per cent, with the committee split and energy-driven inflation keeping cuts off the table for now. For owners, the planning point is not the exact number, it is the message: cheap money is not coming back quickly. If your model assumes a return to near-zero rates to make the numbers work, it is time to rebuild it around the rates you actually have. The businesses that will look strong to a buyer over the next two years are the ones that generate cash and service their own commitments without leaning on falling borrowing costs to bail them out. Read the article here.

AI prompt of the week: are you a platform or a one-off?

With buyers this active, it is worth seeing your business the way an acquirer would. The four things they look for are repeatability, unit economics, low key-person risk, and fit with a fragmented market. Most owners are strong on one or two and weak on the rest without realising it. This prompt forces an honest read before someone else does it for you in a data room.

You are an experienced buy-and-build investor assessing whether my business is a scalable platform or a one-off. I will describe my business: what we sell, how we price and deliver it, our margins and customer-acquisition costs, how dependent the business is on me and a few key people, and how fragmented my market is. Score me out of 10 on each of four signals: 1) repeatable model, 2) strong unit economics, 3) low key-person risk, 4) fragmented-market fit. For each score below 7, give me one specific, practical change I could make in the next 90 days to raise it. Then tell me, in one paragraph, whether you would treat my business as a platform to build on or a single asset to buy cheaply, and exactly what would change your mind. Be blunt.

The four signals that make you a platform, not a one-off

This week’s stories all circle the same question: what makes a business worth building on rather than buying for parts? The infographic below maps the four signals acquirers actually use. A repeatable model that does not depend on you being in the room. Unit economics that hold up as you scale. Low key-person risk, so the business is a platform and not a personality. And fit with a fragmented market full of targets to bolt on. The owners who command premium prices are the ones who can evidence all four. Pick the weakest of the four for your business and spend this quarter strengthening it. That is the work that turns a good company into an irresistible one.

Drop me a line

If one of these struck a chord, or you are weighing up whether to be a buyer or a seller in your own market this year, hit reply and tell me. I read every message. And if a friend or colleague would get something from this, please forward it on to them.

Cheers!

Adam