When workers outpace the company on AI: the Microsoft 2026 verdict

Hi there

Plenty to pour over this week. A live bidding war in Tokyo, a financial giant pulling staff back to five days in the office while also cutting jobs, a Microsoft study that says out loud what most boards already suspect about AI inside companies, and a UK bill that finally gives small suppliers some teeth on late payment. There’s a thread in here about who controls the operating cadence – owners, employees, buyers, or the platforms underneath all of them. Worth a read.

Enjoy!

The brand authenticity gap is now showing up in the numbers

A Forbes Communications Council piece this week argues that marketing has shifted from optimising conversions to defending credibility, and the data supports it. Around 70 per cent of marketers in the latest cohort surveys say AI-generated content is starting to suppress brand trust where it lacks a point of view. The practical implication for owners is that the cheapest content is now actively expensive. The brands that win the next 24 months will be the ones investing in real reviews, named expertise, and content that could not plausibly have been written by a machine. Read the article here.

When private equity ends up in a bidding war you didn’t see coming

EQT launched a $3.76bn tender offer to take Japan’s Kakaku.com private on Wednesday, backed unanimously by the board and by anchor shareholders Digital Garage and KDDI, who together hold around 38 per cent. Within 48 hours, Bain Capital and SoftBank affiliate LY Corp came back with a sweetened $4bn bid. The interesting bit for founders watching this isn’t the price tag, it’s the speed. Japan’s take-private market has gone from sleepy to contested in under a year, and once a buyer brings unanimous board backing, the only thing that flushes out a rival is real cash, fast. Read the article here (paywalled, Archive).

What Fidelity’s five-day mandate is really saying

Fidelity told around 25,000 staff this week they’re back in the office five days a week from September, then announced 800 layoffs in tech and product the same week, plus a hiring push elsewhere. The framing is “evolving operations”. The honest read is a financial services giant deciding that the next phase of growth needs different people in different seats, and using physical presence as the filter. Last week’s issue had Synchrony arguing the opposite case. Both companies are right within their own model. The question every operator should ask is which philosophy fits the work, not which one fits the news cycle. Read the article here (paywalled, Archive).

Microsoft just admitted what most boards won’t

Microsoft’s 2026 Work Trend Index, based on 20,000 workers across ten markets, lands on an awkward conclusion. Employees have figured out how to use AI in their day jobs. Their companies have not. The gap between individual adoption and organisational deployment is now the single biggest predictor of whether AI shows up in earnings. The takeaway for SME owners is the same one that’s been true for every productivity wave since email. The technology arrives bottom-up, but the value only arrives if leadership rewires the workflow on top of it. Most boards are still measuring AI as a cost line. The ones that will pull ahead are the ones treating it as an operating model question. Find out more here.

The UK has finally given small suppliers something to swing

Tucked inside the King’s Speech this week was a Late Payments Bill that gives the Small Business Commissioner real power for the first time. A maximum 60-day payment term, mandatory interest at 8 per cent above base rate on late invoices, and the right to investigate and fine persistent offenders. For any owner of a service or supply business, this changes the economics of carrying a slow-paying enterprise client. It also changes what a buyer will pay for your receivables. Working capital quality is about to move up the diligence list, not down it. Read more here.

What 34,000 small businesses just said about AI and revenue

Intuit’s 2026 AI Impact Report, drawing on 34,000 owner surveys plus anonymised data from 5.3 million QuickBooks businesses across the US, UK, Canada and Australia, found 74 per cent of small businesses using AI report a productivity boost, and notably, AI adoption correlates with hiring rather than cuts. The interesting line for founders is on revenue mix. Owners using AI for finance, marketing and customer service are growing top line faster than non-adopters even after controlling for sector. The “AI replaces people” narrative is still the wrong frame at the SME end of the market. Find out more here.

The other side of the AI-and-jobs story

While Intuit’s data above shows AI correlating with hiring at the SME end, TIME this week ran a closer look at the businesses doing the opposite. Owners of small firms across customer service, bookkeeping, design and copywriting describe replacing one to three roles with AI tooling and not refilling them. The Census Bureau still puts AI usage at under 20 per cent of US firms, and Anthropic’s own research says its models get used for only a fraction of the tasks they could handle. So the macro picture is still slow adoption. The micro picture is sharper. The owners moving fastest tend to be sub-twenty-headcount, owner-operated, and cash-flow conscious, exactly the profile that historically adopts new technology earliest. The hiring-versus-replacing narrative is not either/or. It is a question of where you sit in the curve, and the businesses on the front edge are not waiting for the consensus to catch up. Read the article here.

Why your best managers might be over-correcting on small mistakes

Harvard Business School research featured in HBR this week argues that the instinct to flag every small error in a team’s work is actively counter-productive. The study, by Henrique Castro-Pires, found that letting minor mistakes pass without correction increases overall performance because it preserves the autonomy and motivation of stronger performers. Over-correction signals that judgement is not trusted, which is the single fastest way to turn a high-output employee into a low-output one. For founders this lands at exactly the moment most growing businesses make the wrong move. As the team scales past twenty or thirty people, the founder’s instinct is usually to tighten the feedback loop and add more checking. The HBS read is that this instinct is right for the bottom quartile of performers and wrong for the top quartile. The skill is knowing which conversation belongs in which bucket. Read the article here.

AI prompt of the week: stress-test your pricing for the next deal cycle

Most founders only revisit pricing when revenue softens, which is the worst possible moment to do it. By then the conversation is defensive, and any change reads as desperation to customers and to a future buyer. The point of running this exercise now, when nothing is on fire, is that it gives you a clean view of where your model is brittle, where it is over-engineered, and where you are leaving margin on the table. Drop it into Claude or ChatGPT, give it real numbers, and don’t smooth the inputs.

Act as a pricing strategist who has advised both founders pre-exit and PE buyers during diligence. Here is my business: [paste a 200-word description including total revenue, gross margin, headcount, top three product lines, current pricing model (per seat, tiered, usage, hybrid), top five customers as a per cent of revenue, and net revenue retention]. First, identify the three structural weaknesses in my current pricing model that a sophisticated buyer would flag during diligence and would use to chip price. Second, design two alternative pricing architectures (one consumption-led, one outcome-led) that I could realistically transition into over the next twelve months without breaking my existing book. For each alternative tell me the expected impact on gross margin, the customer segments most likely to churn, the segments most likely to expand, and the one quantifiable metric I should track each quarter to prove the new model is working. Be specific. Avoid generic SaaS pricing platitudes. If consumption pricing would simply not work for my business, say so and explain why.

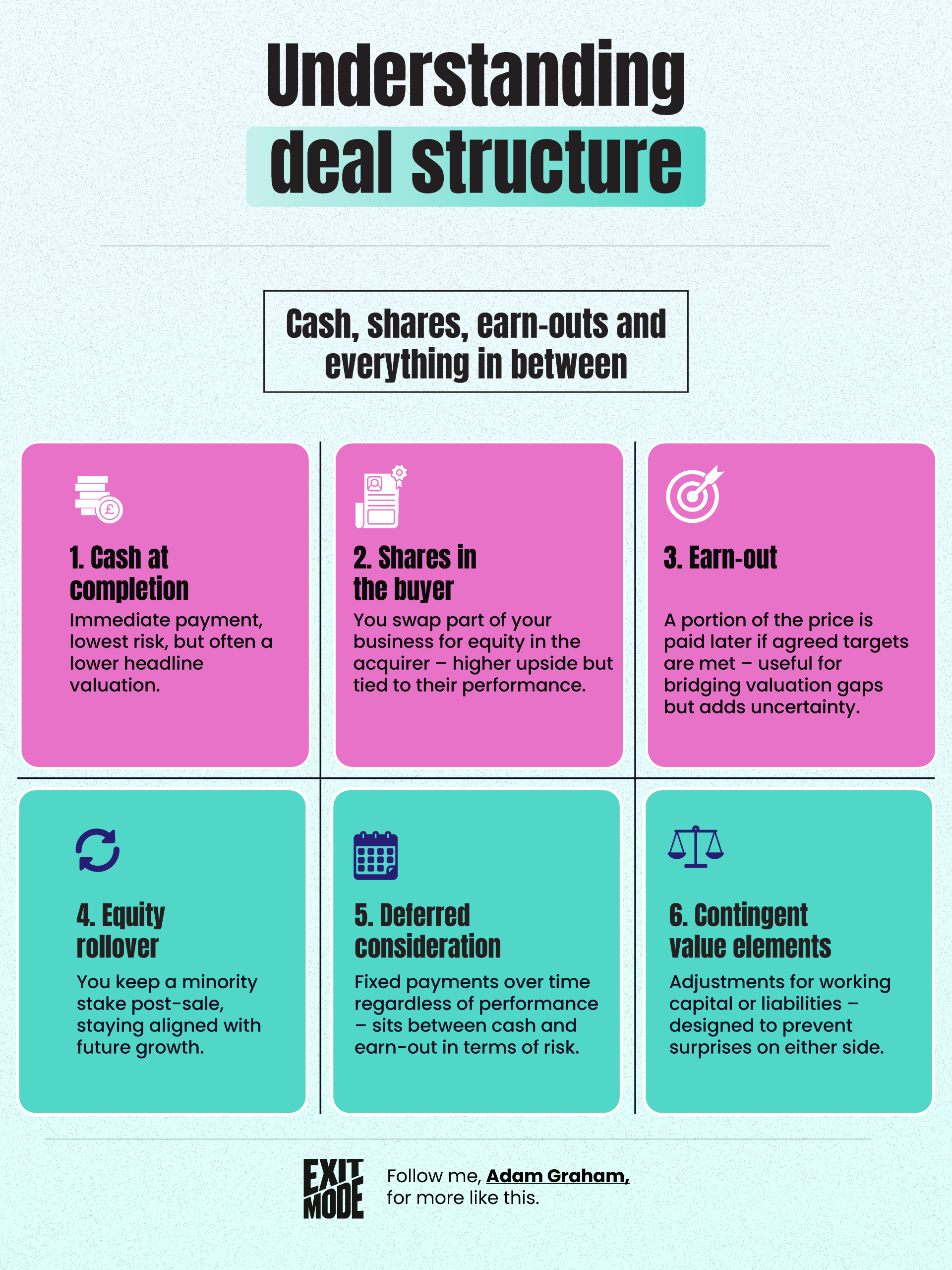

Cash, shares, earn-outs and everything in between

Most founders go into a sale assuming the conversation will be about price. It usually isn’t. By the time you reach the term sheet, the headline number has been pretty well established by the market, and the real negotiation is about structure. The infographic below sets out the six building blocks every offer eventually pulls from: Cash at completion (lowest risk, often a lower headline), Shares in the buyer (upside, but tied to their performance), Earn-out (bridges valuation gaps, adds uncertainty), Equity rollover (a minority stake post-sale, keeps you aligned with future growth), Deferred consideration (fixed payments over time, sitting between cash and earn-out in risk), and Contingent value elements (working capital and liability adjustments, designed to prevent surprises on either side). Knowing which lever the buyer is pulling on, and why, is what separates a clean deal from a painful one.

|

Drop me a line

If anything in this week’s issue lands, or annoys, hit reply. I read everything that comes back, and the conversations have shaped what I write next. Tell me what’s on your desk that wouldn’t make it into a board pack but is keeping you up.

Cheers!

Adam